This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Were major hurricane Erick to trigger the $175 million IBRD CAR Mexico 2024 (Pacific) catastrophe bond that provides disaster insurance to the Mexican government, it could reignite the debate surrounding parametric triggers, given the recency to another trigger event with hurricane Otis back in 2023, Florian Steiger of Icosa Investments has suggested.

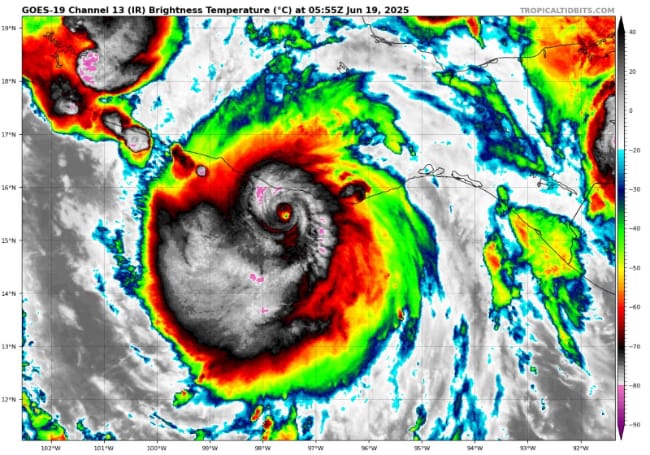

As we reported earlier this morning, hurricane Erick intensified rapidly to become a major category 4 storm, with sustained winds of 140 mph and a minimum central pressure estimated at 939mb.

As we reported earlier this morning, hurricane Erick intensified rapidly to become a major category 4 storm, with sustained winds of 140 mph and a minimum central pressure estimated at 939mb.

As we said in our earlier article, that central pressure was only two millibars above the level needed to activate a partial payout from the IBRD Mexico Pacific coast hurricane catastrophe bond.

However, it’s worth pointing out that a fresh update from the NHC now has the minimum central pressure of hurricane Erick very slightly higher at 940 mb, so now 3 millibar above the trigger pressure.

Update: A further landfall update at 12:00 UTC states that hurricane Erick made landfall with 125 mph sustained winds and a minimum central pressure of 950mb, according to the NHC. So pressure was above the trigger point for the cat bond and did not seem to drop below at any stage as the hurricane approached landfall.

Icosa Investments, the specialist catastrophe bond fund manager, has commented, “Tropical Storm Erick, which formed off Mexico’s Pacific coast, has intensified into a Category 4 hurricane within just a few hours. With sustained winds exceeding 230 km/h, the storm poses an imminent threat and is expected to cause severe damage. Landfall is anticipated later today.

“Unlike in the United States, only a small number of cat bonds cover hurricane risks in Mexico. The current exposure is concentrated in a single IBRD instrument, representing just over 0.3% of market weight. As with most IBRD transactions, this bond relies on a parametric trigger. If the storm’s central pressure at landfall falls below a predefined level, a payout, either partial or total, is made. Such a total loss appears unlikely at present, but it cannot be entirely dismissed, whilst a partial payout is certainly within the realms of possibility as the latest reported pressure is only marginally above the payout threshold.

“Definitive clarity will likely not arrive for several days, because the National Hurricane Center may revise its datasets retroactively. Meanwhile, the bid–ask spread on the affected bond is likely to widen significantly.”

CEO of Icosa Investments Florian Steiger further stated, “Rapid intensification in the Pacific is once again front-page news for cat-bond investors. A fast-strengthening storm now threatens to cause a partial-payout of yet another parametric cat bond, echoing recent experience with Hurricane Otis, which also intensified to major hurricane status within a few hours in almost the same region.

“Such an additional default of a Mexican parametric bond in such short order is bound to reignite debate about trigger design, basis risk and whether the market is truly pricing rapid-intensification exposure. It may also stretch investor patience with parametric structures, whose mixed performance in recent years is already under the microscope.”

You can read all about the IBRD CAR Mexico 2024 (Pacific) catastrophe bond and more than 1,000 other cat bond transactions in the extensive Artemis Deal Directory.

Hurricane Erick threat to Mexico cat bond could reignite parametric trigger debate: Icosa was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

According to SV Chief Financial Officer (CFO) Roland Oppermann, the transaction not only overcame long-standing barriers for the regional German insurer but also paved the way for future capital markets engagement.

According to SV Chief Financial Officer (CFO) Roland Oppermann, the transaction not only overcame long-standing barriers for the regional German insurer but also paved the way for future capital markets engagement.

During a recent interview with Artemis, D’Cunha shared his perspective on how the market is maturing, where innovation is focused, and what it will take to unlock the next wave of capital.

During a recent interview with Artemis, D’Cunha shared his perspective on how the market is maturing, where innovation is focused, and what it will take to unlock the next wave of capital.