This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

A wave of alternative capital, led by a record-setting surge in catastrophe bond issuance, helped reinsurers meet growing demand without pushing prices higher at the July 1 renewals, according to Gallagher Re, as cedants secured improved terms in property and specialty lines.

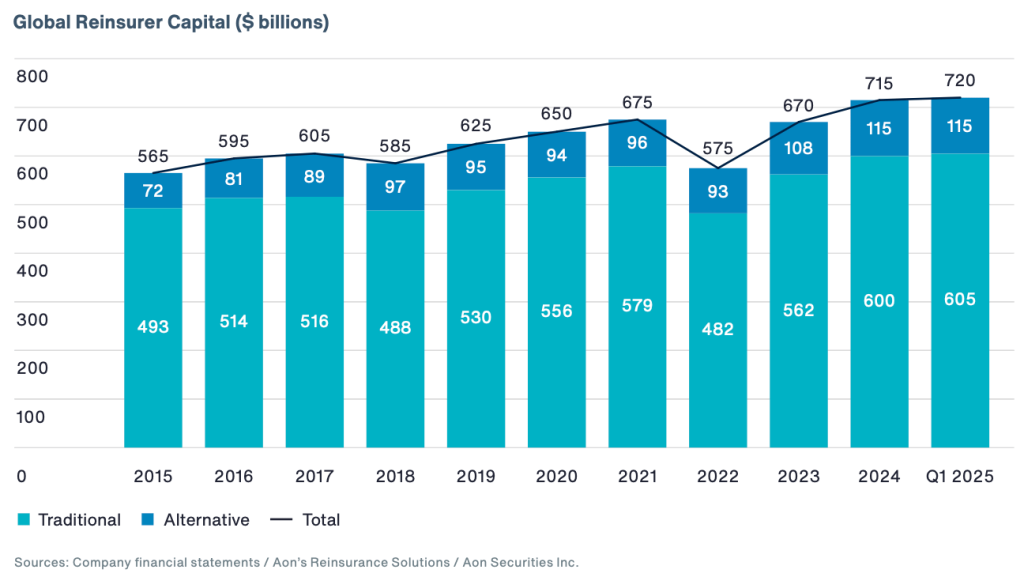

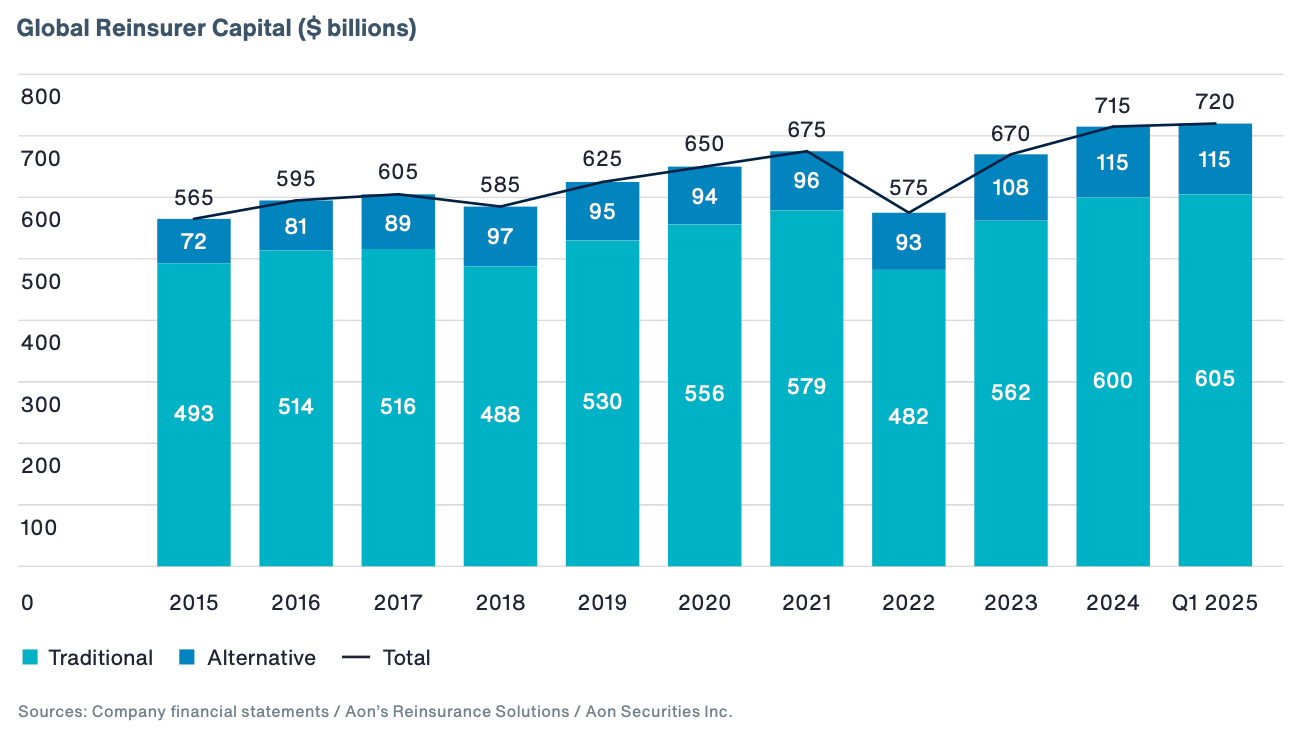

While traditional reinsurance capital reached a new high of $769 billion at year-end 2024, Gallagher Re’s latest 1st View report highlights the critical role of insurance-linked securities (ILS) and cat bonds in sustaining competitive pressure through mid-2025.

While traditional reinsurance capital reached a new high of $769 billion at year-end 2024, Gallagher Re’s latest 1st View report highlights the critical role of insurance-linked securities (ILS) and cat bonds in sustaining competitive pressure through mid-2025.

Issuance so far in 2025, across 144A cat bonds and private cat bonds we’ve tracked, sat at over $17.56 billion for the first half of 2025, which is very close to the Artemis-tracked annual record of $17.7 billion from full-year 2024, as new quarterly issuance records were set in both Q1 and Q2 this year.

According to Gallagher Re, this wave of transactions, driven by strong investor demand and sponsor confidence, ultimately helped reinsurers meet increased demand without pushing prices higher.

Commenting on the July 2025 reinsurance renewals, Tom Wakefield, CEO Gallagher Re, said: “Buyers generally experienced a more competitive reinsurance market at the July 1 renewal compared to recent years, with capacity available even where demand increased, and reinsurers looking to grow.

“Clients were largely able to secure risk-adjusted rate reductions for property treaties and were well-placed to hold pricing broadly flat in casualty lines – in part, as underlying pricing increases continue to flow through to reinsurers.

“With these conditions in place, clients had the opportunity to challenge the status quo, and secure improvements to the structure and terms of their property and specialty reinsurance programs.”

Reinsurers entered the July renewals in “good financial shape” Wakefield noted, with strong 2024 results and ROEs well above the cost of capital.

“Q1 results were weaker due to the impact of January’s unprecedented wildfires in Los Angeles, California, but barring further exceptional cat events, reinsurers remain on track for another good year overall,” Wakefield added.

“As noted in Gallagher Re’s Reinsurance Market Report in April, reinsurers are currently on track to deliver healthy ROEs in the mid-teens for 2025, with traditional reinsurance capital set to increase by another 6% (assuming average results for the rest of the year).”

Despite these fundamentals, cedants achieved risk-adjusted rate reductions of 10–15% on average in property catastrophe programs, particularly for loss-free or structurally enhanced portfolios.

“The increase in reinsurance dedicated capital has been driven mainly by retained earnings at the traditional reinsurance groups, rather than new entrants or capital raises.” Wakefield added.

“We are also collaborating with clients to utilize non-traditional capital vehicles, such as sidecars, where interest in accessing insurance risk remains robust.”

While traditional capital hit new highs, it was the alternative capital layer that gave buyers greater flexibility, helping maintain competitive tension and push back against previously hardened terms.

The cat bond market remained highly efficient, with a Q2 weighted average upsize at 27% indicating investor oversubscription, and a steady market multiple of 3.09, even amid increased issuance.

“The influx of deals in Q2 has been met with ample investor capital, with sponsors continuing to experience deal-upsizes and spread reductions,” Gallagher Re explained.

Gallagher Re also highlighted a 10% increase in property cat sidecar market size since the start of the year and noted that casualty sidecars are gaining traction, with several new entrants accessing the structure in H1.

This marks a growing willingness among ILS investors to engage with more complex and diversified risks outside the traditional property catastrophe space.

Looking ahead, Gallagher Re explained that 2025’s renewals are showing a consistent trend: a market in which the balance of supply and demand has tilted back toward reinsurance buyers.

Reinsurers are increasingly looking to deploy their significant capital, but they remain disciplined in their approach.

Wakefield, added: “Buyers generally experienced a more competitive reinsurance market at the July 1 renewal compared to recent years, with capacity available, even where demand increased, and reinsurers looking to grow.

“With these conditions in place, clients had the opportunity to challenge the status quo, and secure improvements to the structure and terms of their property and specialty reinsurance programs.”

Read all of our reinsurance renewal news coverage.

ILS drives structural flexibility and softer pricing at July renewals: Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.