This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Bridging the widening natural catastrophe insurance protection gap is part of building macro financial resilience, which calls for innovative solutions such as catastrophe bonds, parametric instruments and regional risk pools, according to Lesetja Kganyago, Governor of the South African Reserve Bank.

The G20 South African Presidency, in collaboration with the International Association of Insurance Supervisors (IAIS) and the World Bank Group (WBG), hosted a side event during the G20 Finance Ministers and Central Bank Governors (FMCBG) meetings in Durban in July 2025.

The G20 South African Presidency, in collaboration with the International Association of Insurance Supervisors (IAIS) and the World Bank Group (WBG), hosted a side event during the G20 Finance Ministers and Central Bank Governors (FMCBG) meetings in Durban in July 2025.

The event brought together senior leaders from governments, central banks and supervisors, the private sector, and international organisations to discuss strategies and solutions for narrowing the natural catastrophe insurance protection gap.

The event was opened by Kganyago, who noted that when governments step in with emergency funds or to judge financial reconstruction, it places additional strain on already limited fiscal space.

“For Central Banks, policy makers and supervisors, bridging this protection gap is part of building macro financial resilience. It calls for stronger risk sharing mechanisms, improved data and modelling of climate related risks, and innovative insurance solutions such as parametric instruments, catastrophe bonds and regional risk pools,” Kganyago said.

“More importantly, it requires a coordinated and collaborative effort across governments, insurance supervisors, the private sector, international organisations, multilateral development institutions, and local commodity communities to embed financial resilience into our climate and development strategies.”

He continued: “We must recognise that resilience is not only built in the aftermath of disasters, but in the deliberate and proactive planning, and actions before they occur. Insurance is not a luxury. It is a foundational and critical tool for sustainable development.

“I would encourage all of you to think boldly about how we can address this insurance protection gap beyond innovative products to include appropriate, policies and regulations, that are inclusive, accessible, and tailored to jurisdictional circumstances, especially considering the realities of EMDEs.”

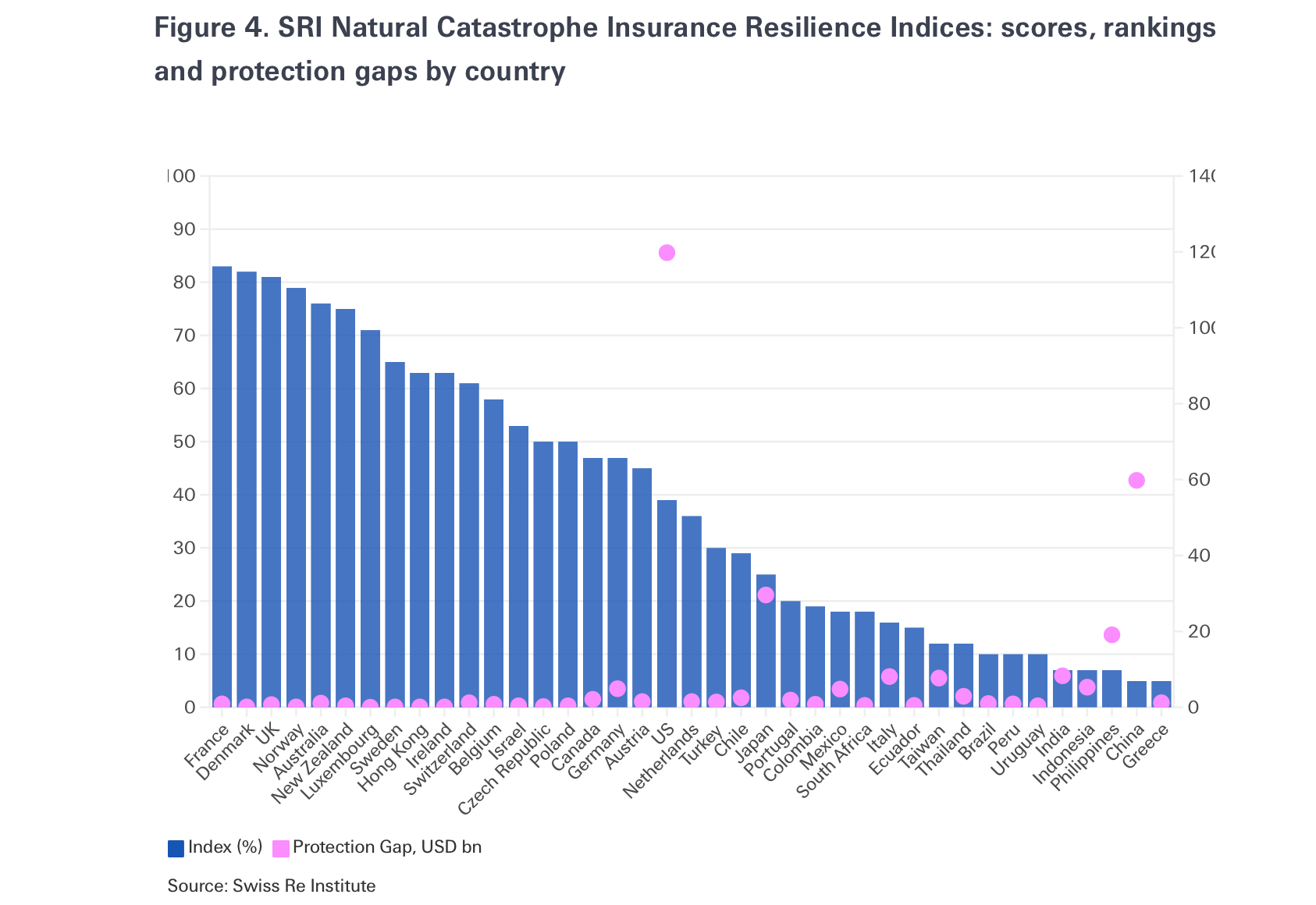

Clearly, the protection gap poses a global challenge, affecting both advanced and emerging market and developing economies (EMDEs).

Going back to 2023, the global insurance protection gap was estimated at 62%, with gaps exceeding 90% in some EMDEs.

Of course, insurers can have a key contribution towards addressing the protection gap, as highlighted by Antoine Gosset-Grainville, Chairman of the Board of Directors of AXA and Member of the Insurance Development Forum (IDF) Steering Committee, one of the panelists from the event.

“Insurers obviously can have a decisive contribution to address the protection gap, through improvement of risk awareness and full innovative insurance solutions. But there are also microinsurance solutions which can be provided and risk transfer mechanisms which have been put in place,” Gosset-Grainville said.

“The second lesson is that prevention and risk reduction require strong public involvement, that’s clear. Co-financing of projects, this is the direction to remove barriers to insurance solution. There are a lot of fields where public bodies can concretely contribute. I’m convinced that at the IDF we can help to discuss and put in place those good options.”

Moreover, Ajay Banga, President of the World Bank, also noted during the event how the catastrophe insurance gap in developing countries is vast, and how this causes for the majority of losses to go uninsured.

“The problem is the insurance gap in the developing countries is vast, and as the governor said when catastrophe strikes, sometimes 90 percent of losses go uninsured. And why is that? Low affordability, limited financial inclusion, underdeveloped markets and weak regulatory and supervisory systems.”

He continued: “Several steps we can take to help and are doing: First, integrate insurance into a broader package of financial services beyond savings and credit deliver it digitally as well. In the whole of Africa where the World Bank supports 13 insurers and 11 financial institutions, are now offering bundled digital services including credit and livestock insurance to over three million farmers, and ranchers in Ethiopia, Kenya, and Somalia.”

Progress is being made towards a new national framework for disaster risk financing and risk transfer in South Africa.

On August 1st, the Treasury announced a Disaster Risk Strategy for the country, which includes accelerating plans towards parametric risk transfer solutions.

“Most public infrastructure is uninsured, placing a large contingent liability on the government,” the South African Treasury explained.

Current municipal insurance pools are seen as too small and limited in coverage, while risk transfer to the private market is a preferred solution.

The Treasury stated, “There is a significant opportunity to build on these facilities to increase asset cover and expand cover to important public infrastructure. The non-life insurance markets in South Africa present a viable opportunity for South Africa to better manage risk by transferring key risks off budget.”

A pilot phase will now begin, with the structure and pricing of insurance products slated to be launched later this year.

The Treasury further explained, “The next steps in the process will be an engagement between Government and the insurance sector on the potential for insurance, particularly parametric insurance, to improve South Africa’s approach to disaster risk. Parametric insurance is index-based insurance, which pays out when an adverse event (such as a flood) occurs. It is increasingly used by governments, municipalities and households to insure against climate-related risk.”

Catastrophe bonds remain a feature of discussions, but the South African government’s new disaster response financing strategy states, “South Africa could also issue a catastrophe bond, which would have the same outcome (payment of a premium for funds only available upon a catastrophic event), but this instrument entails complex documentation and large transaction costs).”

Importantly though, the strategy states that the private sector should be incentivised to innovate in financial resilience to shocks.

There is a key focus on transfer of risk to private capital and while cat bonds are seen as complex and perhaps an instrument for further down the line, it seems likely they will continue to be explored, potentially as mechanisms to source more meaningful capacity to support public infrastructure risk transfer and protection.

Meanwhile, the catastrophe bond markets dramatic transformation, which has been marked by record-breaking growth, expanding risk coverage, and rising global participation was showcased at the World Bank’s recent Innovating for Impact: Scaling Outcome Bonds and Catastrophe Bonds event in Luxembourg.

Cat bonds, parametrics & risk pools can narrow nat cat protection gap: G20 South Africa event was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Speaking at the annual PwC breakfast briefing in Monte Carlo this morning, Henchoz’s comments were a refreshing and realistic scorecard for the industry’s efforts in narrowing protection gaps, as he highlighted that in fact they continue to expand as uninsured losses rise in many cases.

Speaking at the annual PwC breakfast briefing in Monte Carlo this morning, Henchoz’s comments were a refreshing and realistic scorecard for the industry’s efforts in narrowing protection gaps, as he highlighted that in fact they continue to expand as uninsured losses rise in many cases.